The stock market is down a bit, there is unrest in several parts of the world, and interest rates are ticking up. None of these things are great for the housing market.

However there are opportunities. We are seeing some great prices out there, and there is a good level of inventory that will drop off in the next few weeks. If you’re looking to jump in, now is as good of a time as any.

From a historical perspective, sales volume is down, but we still have a great inventory to buy, and prices are also down about 6.5% since this time last year. Currently, we are seeing the median price in line with where it was in 2018 so if you ever wished you would have bought 5 years ago, now your chance to make that a reality.

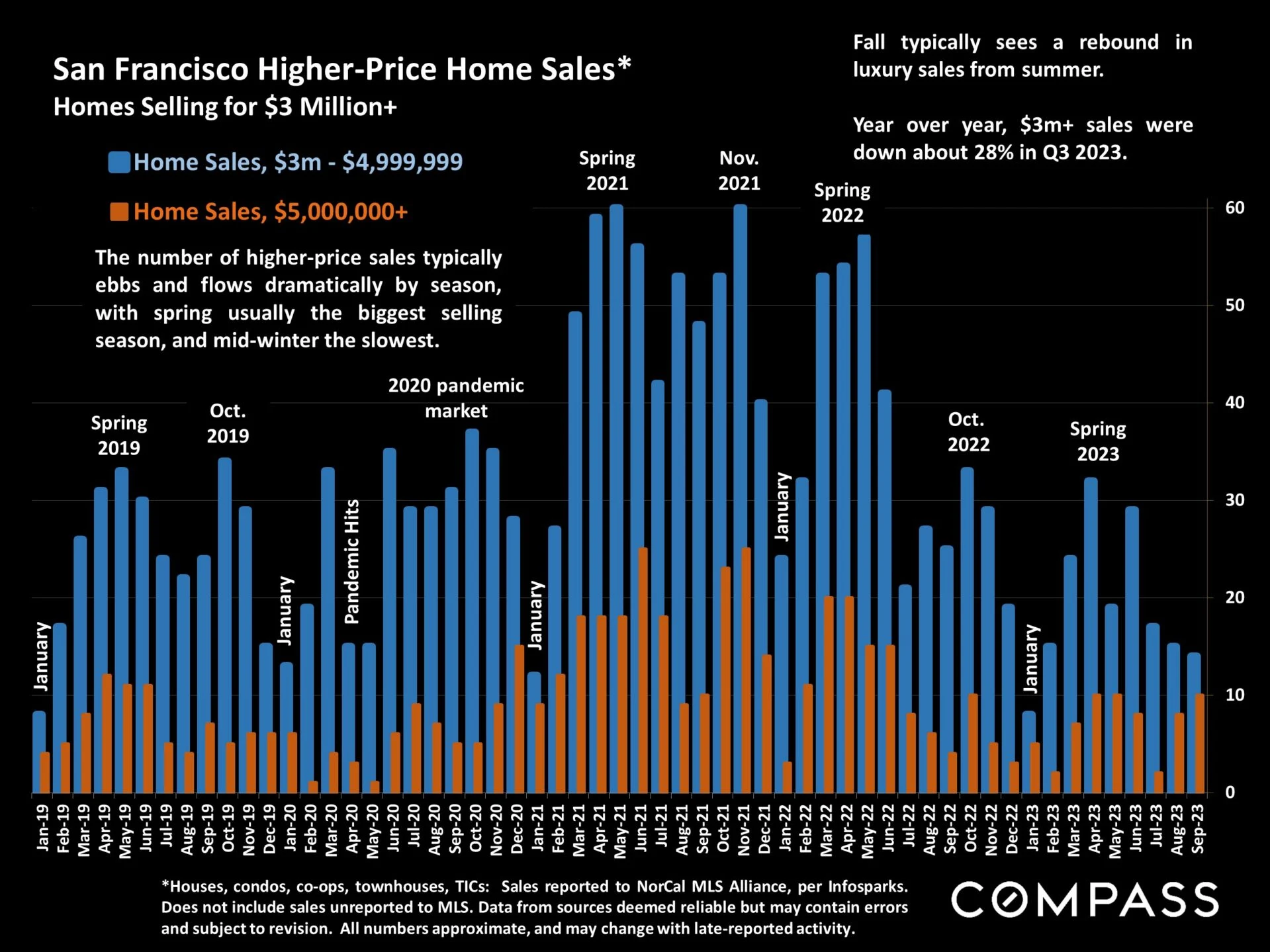

The softest prices are in the under $3-$5M price point, where we have 108 homes for sale and only 51 under contract giving us 6.4 months of inventory. This second softest point is the under $1M mark, where we have about 502 homes for sale and only 150 of them sold, which is around 5.4 months of inventory. There aren’t enough sales to classify the over $7.5M mark, but I will say that it is quite soft in that price point as well.

The Richmond and Sea Cliff lead the way for the biggest drop for median home price, followed closely behind by Bernal and the Mission. For more housing market data keep reading!

Economic indicators have been challenging since the fall selling season began: Interest rates continued to rise through early October and stock markets generally continued to fall from mid-summer, YTD highs. Markets remain volatile and hard to predict, often reacting negatively to positive economic news (such as employment numbers) as they wait for new inflation numbers and try to parse the possible reaction of the Fed. Any definitive impacts on real estate of these recent developments, should they continue, won’t substantially show up until Q4 data begins to become available, and, of course, volatility also means that indicators can turn around quickly.

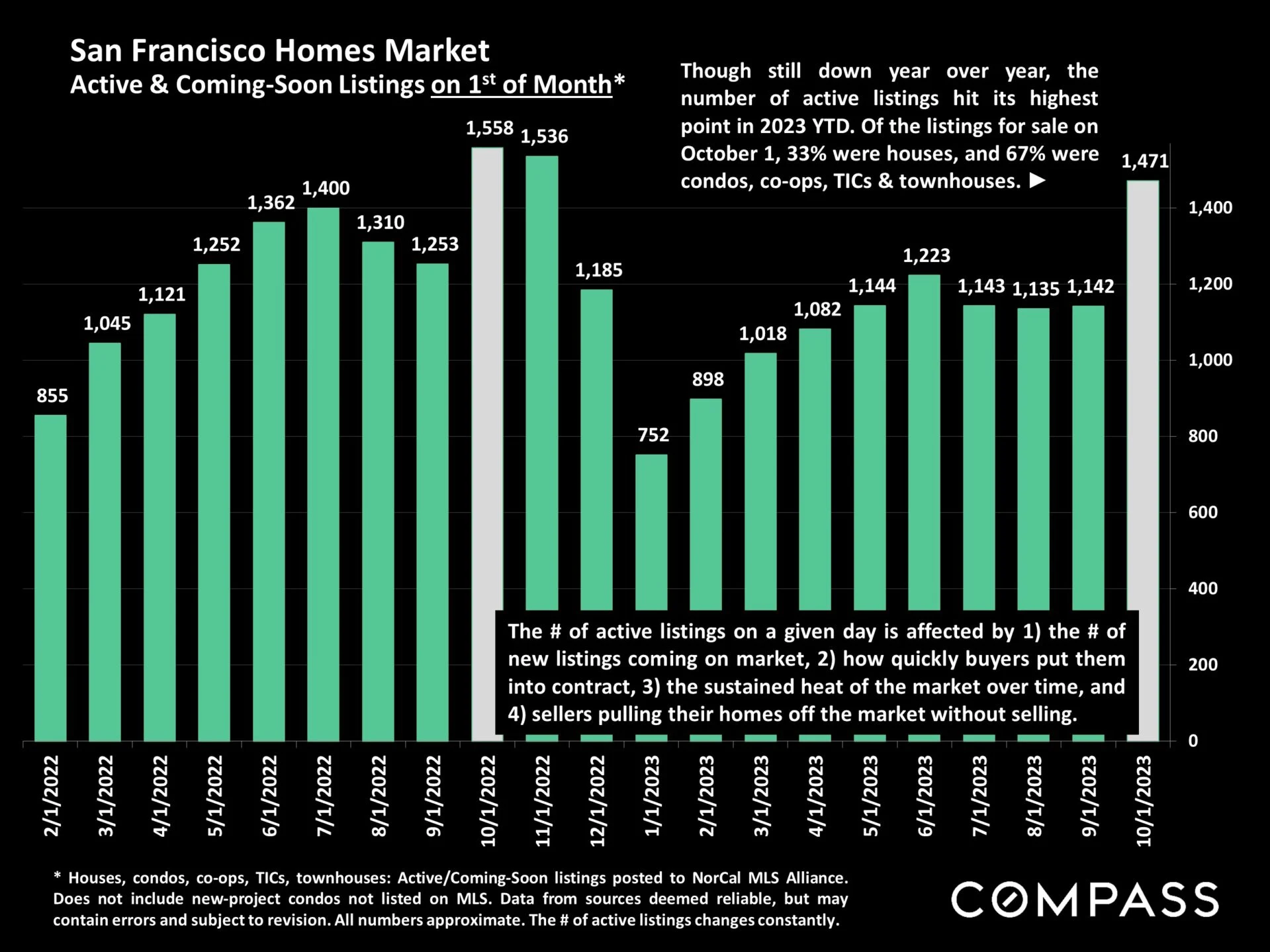

In the meantime, the Q3 median house sales price was down about 6.5% from Q3 2022, and the median condo price down about 4%, but we expect the year-over-year price declines to disappear in coming months. The number of new listings jumped dramatically in September and the total supply of listings for sale just hit a YTD high: This may lead to a substantial increase in sales in October. Supply and demand dynamics remains stronger for houses than for condos, and the downtown condo market is softer than condo markets in other districts of the city. Year over year, the number of home sales in Q3 was down about 22%. The CA Association of Realtors® (CAR) recently issued their initial 2024 market forecast:

CAR forecast: Existing, single-family home sales will increase in 2024 by approximately 23 percent, and the CA median home price is expected to climb by 6.2%. The average 30-year, fixed mortgage interest rate is projected to decline to 6%. Housing supply will remain below normal despite a 10% to 20% increase in active listings, as market conditions and the lending environment continue to improve. [However] the percentage of CA households able to purchase a median-priced single

family dwelling will remain very low by long-term standards.

-CAR Chief Economist, 9/20/23