Despite the ongoing health and economic crisis precipitated by COVID-19, the SF real estate market made a large recovery from the steep declines in March and April. The SF median house price hit a new monthly high in June ($1,800,000), and high-end houses, in particular, have seen very strong demand – this applies to virtually every market in the Bay Area. More affluent buyers – the demographic least affected by COVID-19, unemployment, and also having the greatest financial resources – have been jumping back into the market to a greater degree than other segments.

The condo market has been weaker than the house market, as measured by both supply and demand metrics and median sales price. It may be that prospective condo buyers – often younger and less affluent than house owners – have been more affected by the huge jump in unemployment.

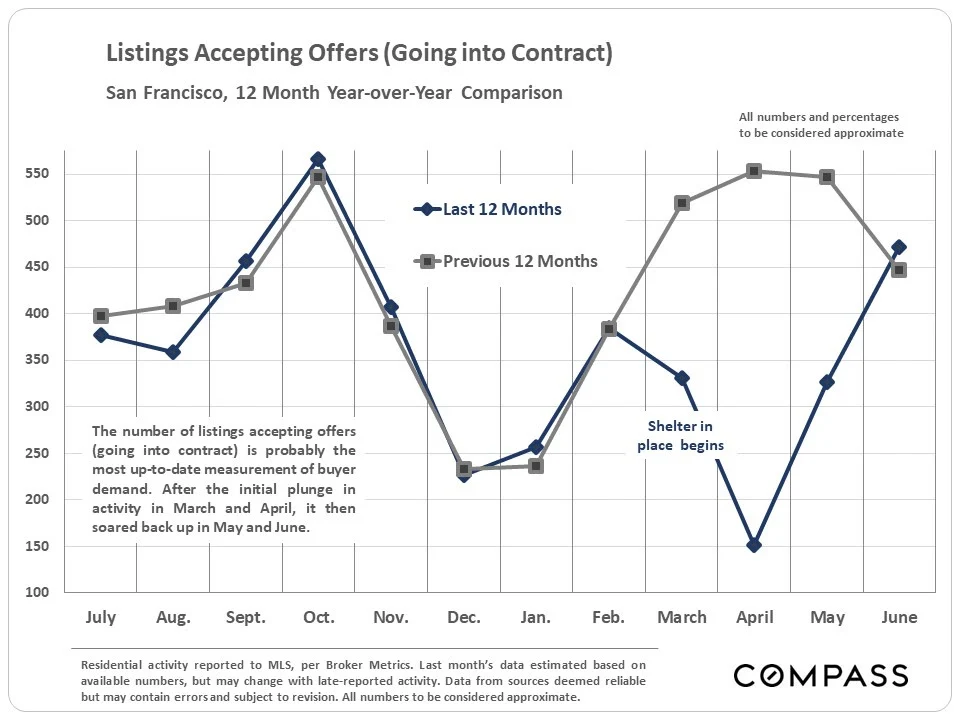

The first chart below illustrates the big rebound in buyer demand, as the number of listings accepting offers in June 2020 rose slightly higher on a year-over-year basis. Of course, closed-sales volume – a lagging indicator – was hammered in Q2 by shelter in place.

High-end sales staged a particularly strong recovery, reaching a new high as a percentage of total sales. This is one of the factors behind the median house sales price hitting a new peak in June.

As illustrated below, the house market (blue line) has performed much better than the condo market (purple line).

Three angles on median home sales price movements – annual, monthly and quarterly. While the median house price has hit a new peak, the median condo price has declined from its 2019 high.

Average days on market remained relatively low in Q2, though higher than Q2 in 2018 and 2019.

The average overbidding percentage declined to zero in Q2 as showing procedures and the offer-making process have been severely affected by shelter in place.

The Bay Area markets with the largest year-over-year increases in the number of listings accepting offers in June 2020 were the 4 outer Bay Area counties of Monterey (up 61%), Santa Cruz (58%), Sonoma (47%) and Napa (37%). They also have among the lowest population densities in the Bay Area. The more urban counties saw more modest y-o-y increases: San Francisco (6%) and Alameda (7%). Other factors may play a role in this: length/strictness of shelter-in-place rules, home price differences, second-home buying patterns, and so on.

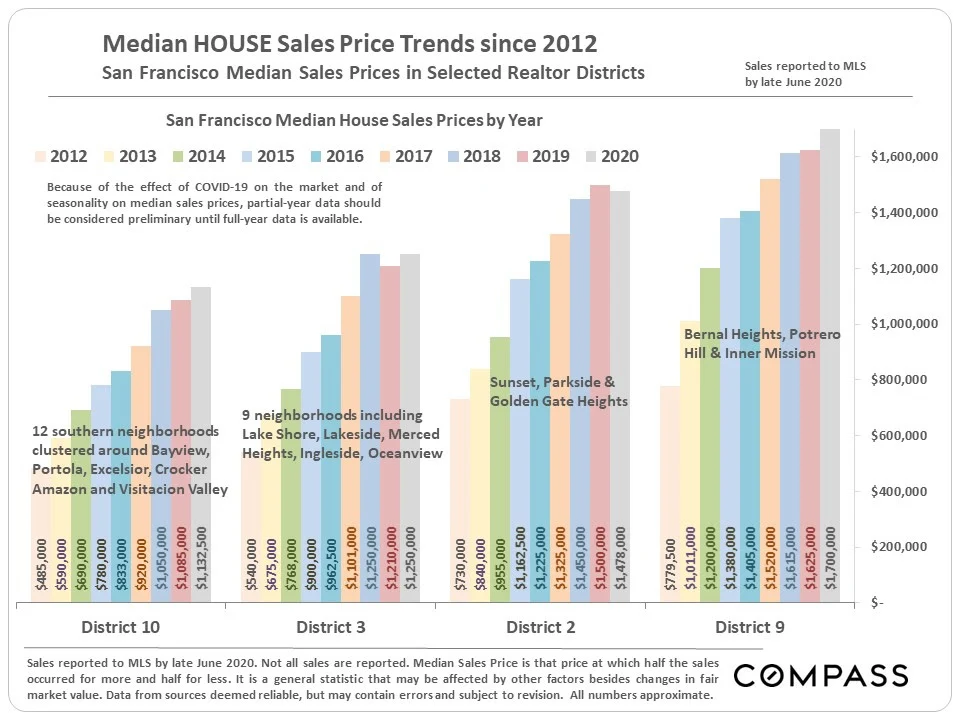

A review of annual and 2020 YTD median home sales prices in some of the largest districts in San Francisco. Changes in median sales price are not perfect indicators of changes in fair market value, as it can be affected by a number of other factors.

Feel free to connect us to anyone you know who has questions about real estate in general. If we can’t help them, we know someone who can. Call us at 415-735-5867 for a no-obligation consultation. You can also email us at info@ruthkrishnan.com.